The stock market broke records and then recently plummeted; unemployment is low, wage growth is sluggish, and the cost of living is increasing. It’s no wonder Americans are stressed about their finances. According to the Federal Reserve, 44% of American adults could not afford a $400 emergency expense or would have to cover it by selling something or borrowing money. For nearly half the adult population, debt remains a persistent concern, while a sufficient retirement nest egg feels unattainable.

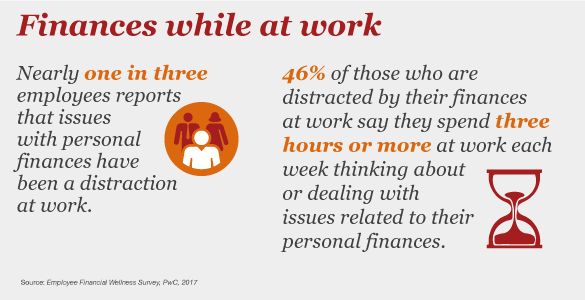

Unfortunately, financial stress isn’t left at the front door of the office. Your employees’ financial woes seep into the workplace and negatively affect their productivity and wellness. A recent study by PwC found that one in three employees reporting financial issues are distracted by these issues at work, and 46% of these individuals spend more than three hours a week dealing with these issues while on the job.

HR professionals need to be more concerned about their employees suffering from continual financial stress and lost productivity at work. An unproductive, disengaged employee can hurt an organization and its customers in ways often not easily seen.

Here are three steps that HR pros can take to help employees understand and better manage their finances.

1. Take a “one-wallet” approach

Health insurance, retirement contributions, voluntary benefits — employers typically approach benefits selection by treating these separately. Companies need to help their employees understand that their benefits selections come from one finite amount of money — their paycheck — which also has to cover housing, insurance, transportation, and day-to-day spending.

How? Start by offering access to a recommendation engine within your benefits portal; this is a benefits selection tool that helps employees view their benefits elections, including some retirement finances, with a one wallet approach during the election process. (My company offers one.) It pools together their health and financial needs when employees choose their benefits. This intuitive technology helps employees see the full suite of benefits that are available, and asks targeted questions covering emotional, physical, and financial health to provide a responsive, personalized recommendation for each individual employee. As most Americans will admit to struggling to understand their financial assets and commitments, this approach can save employees money by asking the right questions to help them determine what benefits they need and what they don’t. It also provides employees with peace of mind that they’re managing the financial issues they are facing today, as well as whatever hurdles tomorrow may bring based on their particular life stage.

2. Be mindful of life stages across generations

The American workforce today comprises an unprecedented five generations, and millennials now account for one of every three U.S. workers. This means your employee spectrum covers a wide variety of life stages, and their corresponding financial concerns are equally as varied. While one may be starting his or her first job out of college and trying to deal with student debt, another is welcoming their first child, and another may be planning for retirement.

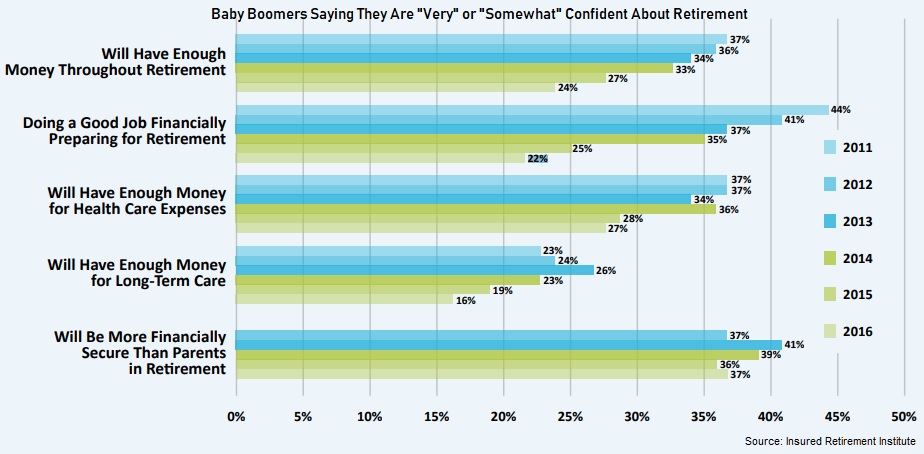

Employers need to be aware of these differences and understand the best way to communicate with each generation to meet their specific needs. For example, only 22% of Baby Boomers believe they’re doing a good job financially preparing for retirement. Since Boomers generally prefer face-to-face assistance, setting up small group sessions on retirement planning can be an effective way to engage this generation. Conversely, mobile-friendly content that can be consumed wherever and whenever will appeal to millennials, who are more likely to view their job as a part of their identity and consequently blur the lines between workday and personal time. When researching student loan debt assistance or pet insurance, millennials will want to access this helpful information at times that may not coincide with a traditional workday. This type of awareness about generational differences and life stages will help employers tailor communications, both for the various types of financial issues facing their workforce and the different ways employees prefer to engage with information.

3. Offer carrots, not sticks

Can you entice employees to make better financial decisions? The answer is an unequivocal “yes.” From banks to trucking firms, corporations across the U.S. are implementing financial wellness programs, which teach employees money-management skills and strategies for saving. Some of these programs use personal consultations with financial professionals, while others utilize online and mobile tools. Many provide a financial incentive — anywhere from a few tens of dollars up to a few thousand per employee — if workers actively save money, pay down debt, or take a financial literacy course.

The recent tax bill offers another opportunity to instill healthy financial habits in your employees. Numerous companies are investing in expanded benefits following the reduction of the corporate tax rate. Increasing your 401(k)-match amount, or even giving employees a lump payment in their retirement accounts, can encourage greater saving and drive awareness with employees about how their nest eggs are faring.

It’s no secret that financial issues can be daunting and oftentimes stressful. As HR professionals, you have the opportunity to make a difference in your employees’ lives by providing the right tools, tailoring messages, and giving them innovative technologies for wise benefits selections. This also enables you to re-engage and enhance the power of your workforce, subsequently making a positive impact on your company’s goals.